Global Economic Slowdown Triggered by US Tariff: In a world still reeling from the economic aftershocks of the pandemic and geopolitical instability, the latest US tariff policies are adding another layer of complexity. According to Swiss Re Institute’s World Insurance sigma report, global GDP growth is projected to decelerate from 2.8% in 2024 to 2.3% in 2025. This significant dip in economic performance is attributed primarily to the introduction of protectionist US trade policies. The resulting reduction in global trade and heightened economic uncertainty has led to a cautious response from businesses and consumers alike, who are cutting back on investments and expenditures.

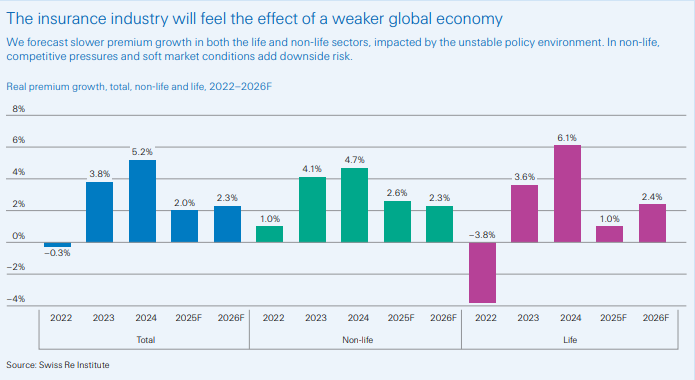

Insurance markets are mirroring this trend. Global insurance premium growth is expected to slow to 2% in 2025—down from 5.2% in 2024. Both life and non-life insurance sectors are witnessing reduced demand, particularly in regions hit hardest by the tariffs, like the US. The knock-on effect of tariffs has significantly raised the cost of imports, impacting sectors like motor insurance and construction. While inflation-adjusted claims remain within manageable limits, there is a clear shift toward more fragmented and protectionist markets. This fragmentation could reduce the affordability and availability of insurance in the long term.

Despite this downturn, there is a silver lining for insurers. Rising investment income is cushioning the profitability blow. Some market segments, such as credit, surety, and marine insurance, may find new opportunities amid global supply chain realignment and policy-driven fiscal stimulus. In regions like China and the EU, supportive monetary policies and expansionary government spending could create conditions ripe for selective insurance growth, especially outside the US.

Who Can Apply for Coverage in Tariff-Affected Insurance Lines?

Individuals and businesses based in the United States and engaged in sectors like automotive, construction, manufacturing, and trade are especially advised to review their insurance policies. Motor vehicle owners, construction companies, import/export firms, and logistics service providers are among the most affected. These groups should consider revisiting their current policies or applying for new coverage tailored to economic disruption risks, such as credit and surety insurance.

Insurance providers are also encouraging individuals and small enterprises with exposure to international trade to consult with insurance advisors. These stakeholders can benefit from specialized products that protect against delayed deliveries, contract breaches, or geopolitical risk escalations tied to the new tariffs.

Insurance Fees and Premium Adjustments in 2025

In 2025, insurance premiums across most sectors are expected to reflect increased operational costs. For motor insurance in the US, particularly physical damage coverage, prices are likely to increase due to higher costs for imported parts and vehicle replacement. Swiss Re projects that motor repair and replacement expenses will grow by 3.8% in 2025, driven largely by import tariffs.

While this increase is considerably lower than the post-COVID inflation spike, it still marks a substantial deviation from pre-pandemic norms. Commercial lines may see softened pricing due to competition, but select specialty products like marine and credit insurance could see premium adjustments upward due to elevated risk exposure.

How to Use Insurance Products to Offset Tariff Risks

Insurance can serve as a strategic buffer against the financial uncertainties introduced by tariffs. Here’s how:

- Credit & Surety Insurance: Protects businesses from default by trading partners or delayed payments in volatile markets.

- Marine Insurance: Covers shipping-related risks, particularly useful in diversified or redirected trade routes post-tariff.

- Business Interruption Insurance: Offers protection against lost income from supply chain disruption.

- Motor Physical Damage Coverage: Essential for consumers as vehicle repair costs surge due to higher auto part tariffs.

In this climate, comprehensive policy review and realignment with current risk levels are key. Engaging with insurers to tailor coverage to tariff-specific risks is highly recommended. Swiss Re Institute Official Site

How to Apply for Tariff-Responsive Insurance Policies

Applying for specialized insurance coverage is straightforward but requires strategic planning:

- Assessment of Exposure: Determine how tariffs directly or indirectly affect your operations or assets.

- Consultation with Insurance Advisors: Seek professional advice to identify coverage gaps.

- Compare Offers: Use online comparison tools or brokers to assess the best deals based on risk exposure and geography.

- Documentation: Prepare relevant financial statements, trade records, and compliance documents.

- Submit Application: Apply online or through agents, depending on the insurer’s protocol.

Important Dates to Remember

| Event | Date |

|---|---|

| Swiss Re Institute Report Published | 9 July 2025 |

| Expected Tariff Adjustments | Q3 2025 |

| Premium Rate Adjustments Start | August 2025 |

| Policy Review Recommended By | September 2025 |

| Insurance Outlook 2026 Forecast Release | January 2026 |

Disclaimer

This article is for informational purposes only and does not constitute financial or insurance advice. Readers are encouraged to consult licensed insurance advisors or financial professionals before making decisions based on the information provided. All data and forecasts mentioned are attributed to Swiss Re Institute and are subject to change based on evolving market conditions and policy decisions.

Also read: Experior Financial Group USA Unveils Agent-Centric: Platform to Maximize Life Insurance Success

Global Economic Slowdown Triggered by US Tariffs Conclusion

The global economy is entering a period of heightened volatility driven by aggressive US tariff policy. Swiss Re Institute’s findings underline a clear trend: slower economic growth, diminished trade, and a cautious insurance sector bracing for higher claims and reduced premiums. While the broader insurance market is seeing a slowdown, pockets of opportunity remain for forward-thinking insurers and policyholders willing to adapt to this changing environment.

Motor insurance in the US is likely to face the sharpest impact, especially in physical damage claims due to rising auto parts costs. However, this does not spell doom across the board. Insurers can offset declining premiums through higher investment income and expansion into emerging risk protection products. Marine and credit insurance, for example, are expected to gain relevance as global trade patterns shift.

Consumers and businesses must take proactive steps. Reviewing existing coverage, understanding new tariff-related risks, and seeking tailored insurance solutions can significantly improve financial resilience. As the world becomes more fragmented, insurance will continue to play a vital role in buffering economic shocks—provided it’s used strategically.

As we look forward to 2026, stabilizing labor markets and fiscal stimulus in certain regions may offer a rebound. Yet, the long-term implications of a fragmented global market require agility from both insurers and policyholders alike. Risk resilience in this new world depends on adaptability, innovation, and informed decision-making.

Global Economic Slowdown Triggered by US Tariffs FAQs

1. How do US tariffs directly affect the insurance industry?

US tariffs increase the cost of imported goods like auto parts and construction materials. This raises claims costs in sectors such as motor physical damage and construction insurance, while also lowering overall demand due to inflation-driven consumer spending cuts.

2. Which insurance sectors are most impacted by the 2025 US tariffs?

The most directly affected sector is US motor insurance, especially physical damage claims due to higher auto parts costs. Construction and import-related lines also face pressure. However, opportunities may rise in credit, surety, and marine insurance outside the US.

3. Will insurance premiums continue to rise in 2026?

Swiss Re forecasts a slight rebound in premium growth to 2.3% in 2026. This uptick depends on how economies adjust to the “new normal” of tariffs and how much fiscal and monetary support is injected into markets like the EU and China.

4. What strategies can policyholders use to mitigate tariff-related insurance risks?

Policyholders should review and adjust their insurance coverage, explore specialty products like business interruption and credit insurance, and consult with brokers to realign protection based on new risk factors introduced by tariffs and supply chain disruptions.

5. Are there benefits to the insurance industry despite the global slowdown?

Yes. Rising investment income, increased risk awareness, and the growth of niche products like trade credit and marine insurance present opportunities. Insurers that adapt quickly can leverage these changes to maintain profitability and expand coverage offerings.